Why Statutory Interest Rarely Works, and What Does

The Late Payment of Commercial Debts (Interest) Act 1998 lets you charge late-paying business customers 8% above base rate, plus a fixed compensation amount of £40 to £100 per invoice. SAFE Billing Platform will calculate the interest automatically and add it to the customer’s account if you turn the feature on.

Almost nobody turns the feature on. After two decades of running this platform for UK telecoms resellers, the honest pattern is that statutory interest is a feature people are pleased to know exists and rarely actually charge. The thing that recovers cash is automated dunning letters, sent on a predictable schedule, with the wording stepping up each time.

This post explains both. The interest mechanics, because they are useful. The dunning sequence, because it is what works.

Key Takeaways

- Statutory interest under the 1998 Act is 8% over Bank of England base rate plus £40 to £100 per invoice (GOV.UK guidance, 2025)

- SAFE calculates it automatically; the feature is off by default

- Most customers leave it off because the relationship cost outweighs the marginal recovery

- A three-letter dunning sequence at fixed intervals recovers more cash than interest charges

- Recovery rate correlates with the number of touchpoints, not the rate of interest

- The wording should step up: friendly reminder, formal notice, final demand with stated next steps

Key terms in this article

What is statutory interest?

Statutory interest is the rate of late-payment interest set by the Late Payment of Commercial Debts (Interest) Act 1998. It is 8% above the Bank of England base rate at the time the debt became overdue, plus a fixed compensation amount of £40 to £100 per invoice depending on the size of the debt.

What is a dunning letter?

A dunning letter is a reminder sent to a customer with an overdue invoice. The word “dunning” comes from the practice of repeatedly asking for payment. Modern dunning sequences are usually a series of three or four letters at fixed intervals, with the tone escalating from friendly reminder to final demand.

What is aged debt?

Aged debt is the money your customers owe you, broken down by how long it has been outstanding. The buckets are usually 0-30 days, 31-60 days, 61-90 days and 90+ days. The older the debt, the harder it is to collect.

How Statutory Interest Works in SAFE

If you decide to charge statutory interest, SAFE handles the calculation. The configuration is per customer or per customer group, and the feature is off by default.

When an invoice becomes overdue:

- SAFE flags it as eligible for statutory interest after the agreed payment terms have elapsed.

- Interest accrues daily at 8% over the Bank of England base rate on the date the debt became overdue.

- The fixed compensation amount is added based on invoice size: £40 for invoices up to £999.99, £70 for £1,000 to £9,999.99, £100 for £10,000 and above.

- The accrued interest appears as a line item on the customer’s next invoice.

The rate of 8% over base is generous to the supplier. With base rate at any normal level, the effective annual rate is 12 to 13%. On a £5,000 invoice paid 90 days late, that is roughly £150 of interest plus £70 of fixed compensation. Meaningful money on paper.

Why Almost No-One Turns It On

The actual recovery from charging statutory interest is small, and the relationship cost is large.

The customer is not surprised they owe interest. They are surprised the supplier they have worked with for five years suddenly cares enough to claim it. The relationship signal is “I no longer trust you to pay me”, and the customer reads it that way.

The interest is rarely paid. Customers who pay late routinely will look at the interest line item, ignore it, and pay the original invoice. Chasing the unpaid interest then takes more letters than chasing the original invoice ever did.

It works once on a customer you are willing to lose. As a tool of last resort against a customer you are about to fire, statutory interest works. As a routine billing practice across a portfolio of customers you want to keep, it does not.

From our experience: the customers we have who run with statutory interest enabled are in two camps. The first camp uses it as a credit-control signal: they invoice with the clause visible but only ever switch the calculation on for specific accounts in dispute. The second camp tried turning it on across the board, had a difficult quarter of customer pushback, and turned it off again. The realistic adoption rate across our customer base is in the low single digits.

What Actually Recovers Cash

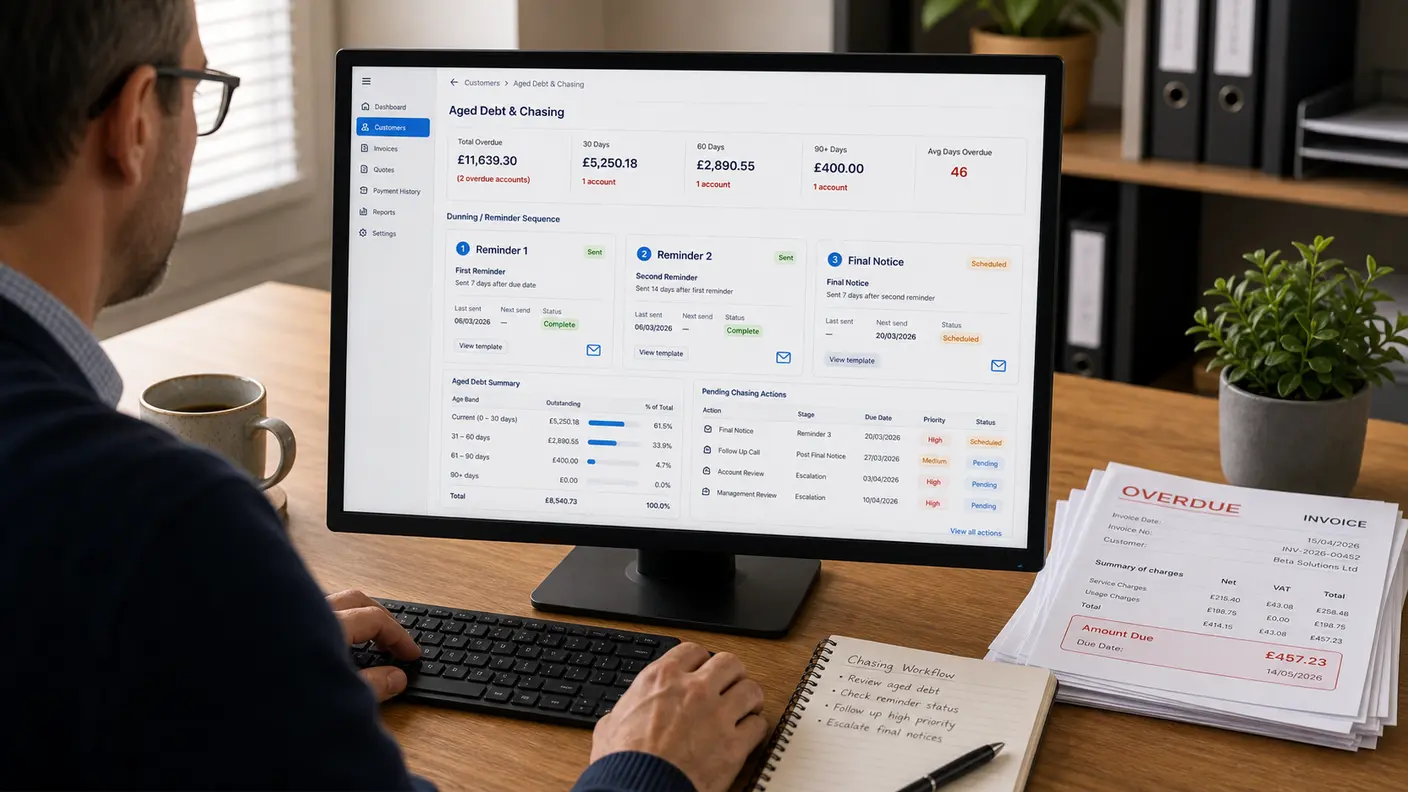

A semi-automated dunning sequence, sent on a predictable schedule, with the wording adjusted by debt age. The mechanics are unglamorous. The results are reliable.

A typical sequence:

Letter 1, friendly reminder, 7 days after due date. A short note: invoice X, dated Y, was due on Z and remains unpaid. If payment has crossed in the post, please ignore this. Otherwise, please remit at your earliest convenience.

Letter 2, formal reminder, 21 days after due date. A firmer note: invoice X is now 21 days overdue. Please remit within 7 days. If there is a query, please contact us directly.

Letter 3, final notice, 35 days after due date. A formal final notice: invoice X is now 35 days overdue. If payment is not received within 7 days, the account may be passed to debt recovery and services may be suspended.

Phone call, 50 days after due date. Automation stops being enough. The reseller picks up the phone.

The exact intervals vary by reseller and customer base. The principle is consistent: predictable timing, escalating tone, clear next step.

Why the Sequence Works

Three reasons.

Most overdue payments are administrative, not deliberate. The invoice missed someone’s payment run, sat in a filtered inbox, or was approved but never released. A first reminder catches most of these.

The escalation is psychologically real. Letter 1 is friendly and easy to ignore. Letter 3 is harder to ignore because it implies the supplier has a follow-through plan. Most customers settle between Letter 2 and Letter 3.

Phone calls work when letters do not. By the time the sequence reaches a human call, the customer either has a real problem to talk about or has been deliberately stalling. Either way, a call resolves it faster than another letter.

Configuring Dunning in SAFE

The sequence is configured per customer group, with the letters written as templates that pull in invoice details automatically. The billing run guide covers the dunning step as part of the monthly cycle. A few specific configuration notes:

- Letter templates can be customised per customer segment. Different tone for residential customers, business customers and reseller channel partners.

- The trigger is days past due, calculated automatically.

- Send method is normally email, configured per template per customer segment.

- Customers in dispute can be flagged to pause automated chasing without removing them from aged-debt reports.

- Sequence reset rules are configurable: a part-payment can either reset the sequence to letter 1 or hold it at the current stage.

Aged Debt as the Reseller’s Real Metric

The point of all of this is the aged debt position, not any individual interest charge. A reseller running a clean dunning sequence will have most of their aged debt in the 0-30 day bucket, very little above 60 days, and almost nothing above 90. A reseller without one will have the opposite pattern.

The late payment crackdown post on safeonlinebilling.com covers the wider 2025-26 regulatory context, including the cap on payment terms and the new Small Business Commissioner powers. The point on this side of the conversation is what the reseller actually does in the billing run, week to week.

How SAFE Handles It

Aged debt reports are built into the KPI screens. The dunning sequence runs as part of the monthly billing run. Statutory interest is available if you want it, off by default, configurable per customer group. The combination is what most resellers actually use.

For a walk-through against your own current aged debt profile and a sample letter sequence, the contact form is the way in.

Dr Paul Barrass

Founder & Technical Director, Safe Online Billing

Paul founded Safe Online Billing in 2005 and has built telecoms billing software for UK resellers for over 20 years. About the team →